Understanding what a Power of Sale is and how it works is crucial for homeowners facing financial difficulties. If you’re struggling with mortgage payments, knowing how to stop a Power of Sale can protect your home and finances. This process allows lenders to recover their money by selling your home when you default on your mortgage. To prevent a Power of Sale, understand the different types of lenders and how they operate.

What Is Power of Sale?

Power of Sale is a legal action that a lender takes when you have defaulted on your mortgage or home equity loan. In this process, the lender seizes control of your home and sells it to recuperate their money. You may receive the remaining sale money, but only after legal, real estate and mortgage-related fees are paid.

In a Power of Sale, the lender controls the sale of the property but does not take over the title. It is easy to confuse this process with the term “foreclosure” which is when the lender gains full ownership of the property and they can do what they want with the property including selling it and keeping all the proceeds.

The Power of Sale Process in Ontario

Understanding the steps your lender must follow is crucial to preventing home loss through a Power of Sale. Find out what the requirements are to get your payments in order or to negotiate new payments with your lender. Seeking legal advice is also recommended.

The Power of Sale process has four steps: notice of sale, statement of claim, writ of possession, and eviction notice. These are further explained below.

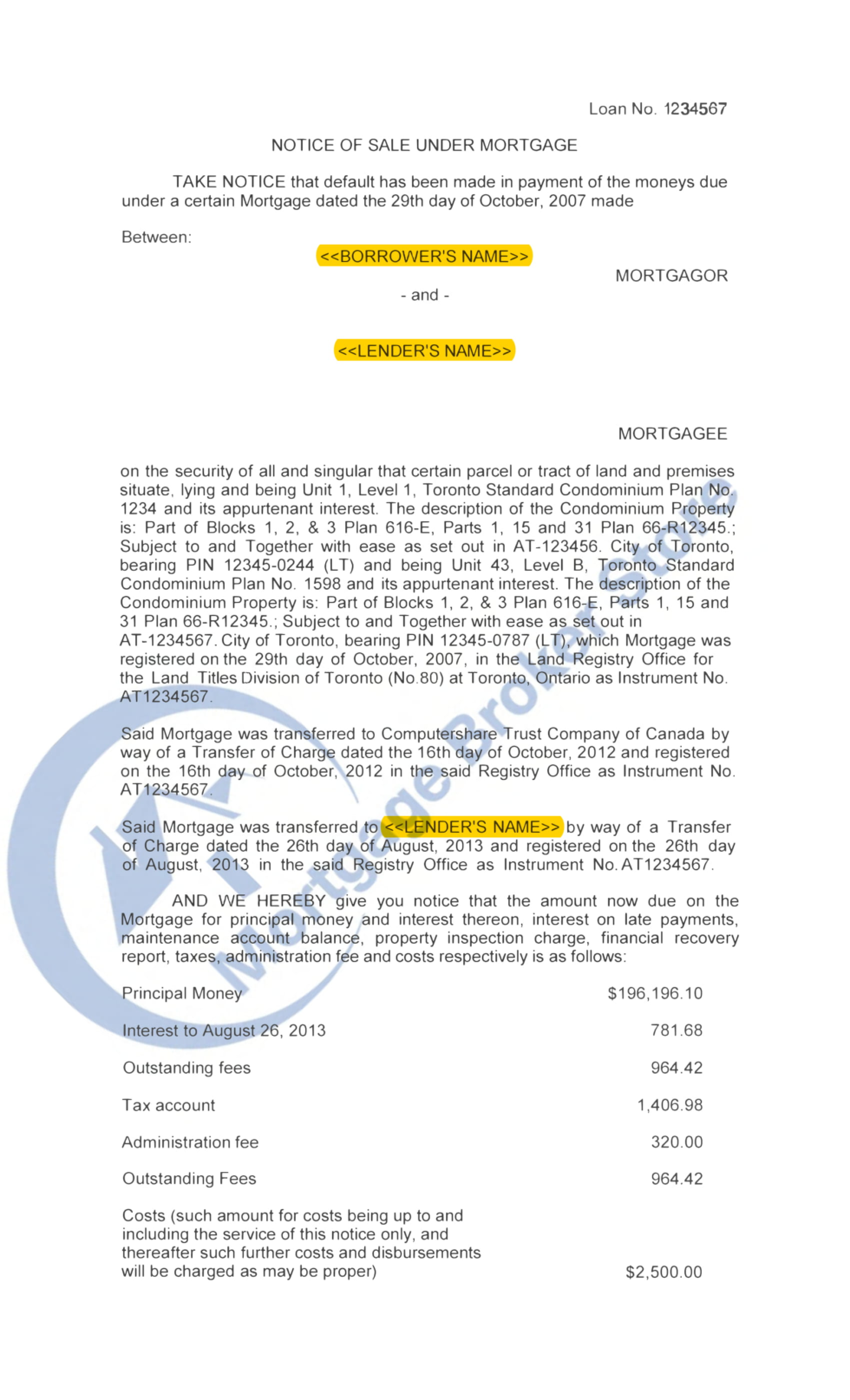

Notice of Sale

In many loan or mortgage agreements, the lender can initiate Power of Sale 15 days after you miss a payment. The lender sends you a legal document called notice of sale, which is also filed in court.

A notice of sale states the mortgage default and outlines what must be paid to halt the Power of Sale. After receiving this document, you usually have 35 to 40 days to repay your lender. This is known as the redemption period.

During the redemption period, you can try to negotiate with your lender. Depending on your lender and loan agreement, you might need to repay the entire loan, not just missed payments. You will likely be required to pay the lender’s legal fees to file the notice of sale.

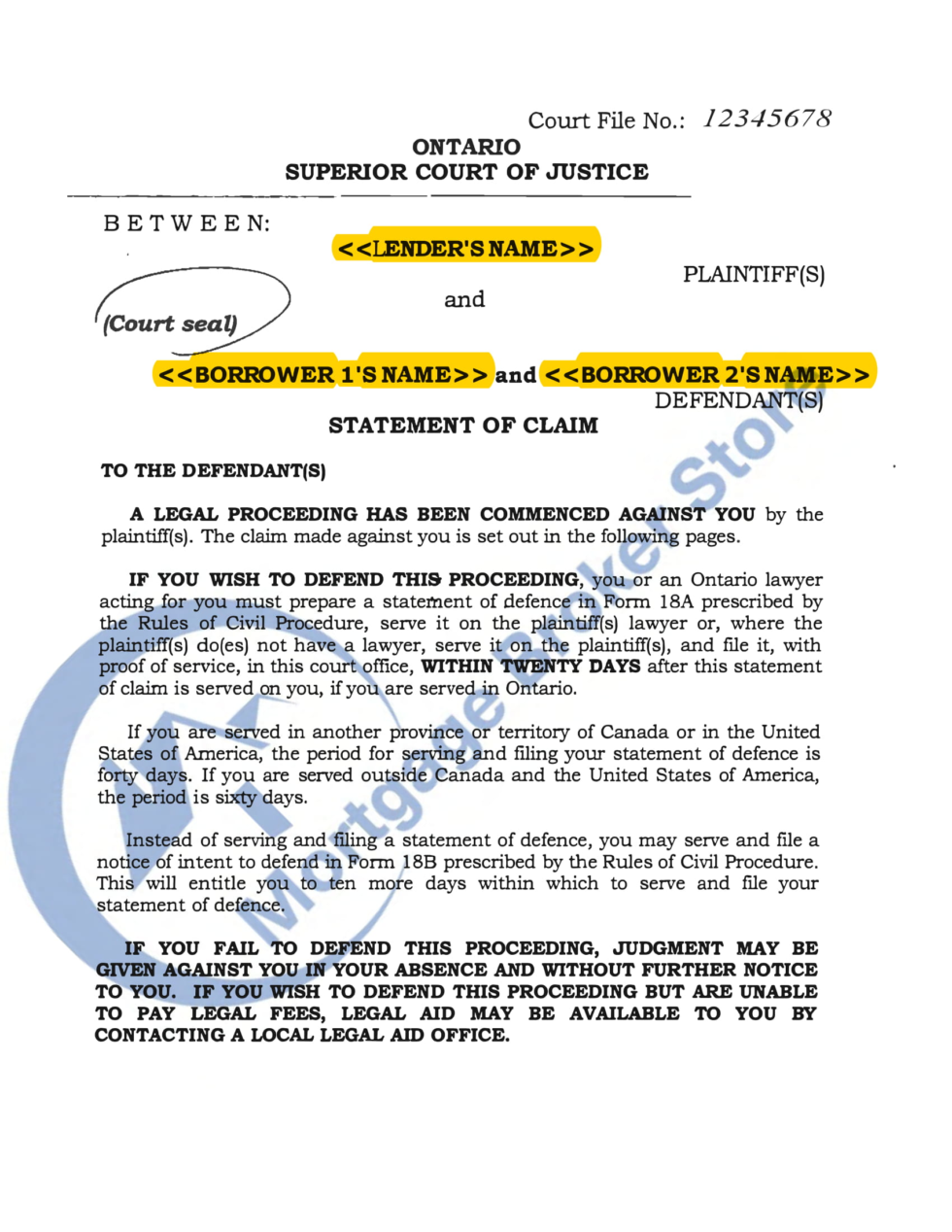

Statement of Claim

If the redemption period expires without repayment or another resolution, you will receive a statement of claim, which describes the evidence the lender has against you.

Upon receiving the statement of claim, you have about 20 days to respond with a statement of defence, which can list your reasons not to pay some or all that the lender is demanding and any counterclaims you may have.

Only proceed with a statement of defence if you have a strong case against your lender, such as if they have violated the loan agreement by changing your interest rate on a fixed-interest loan or failing to provide the agreed funds.

Losing a statement of defence in court can result in penalties of up to $30,000.

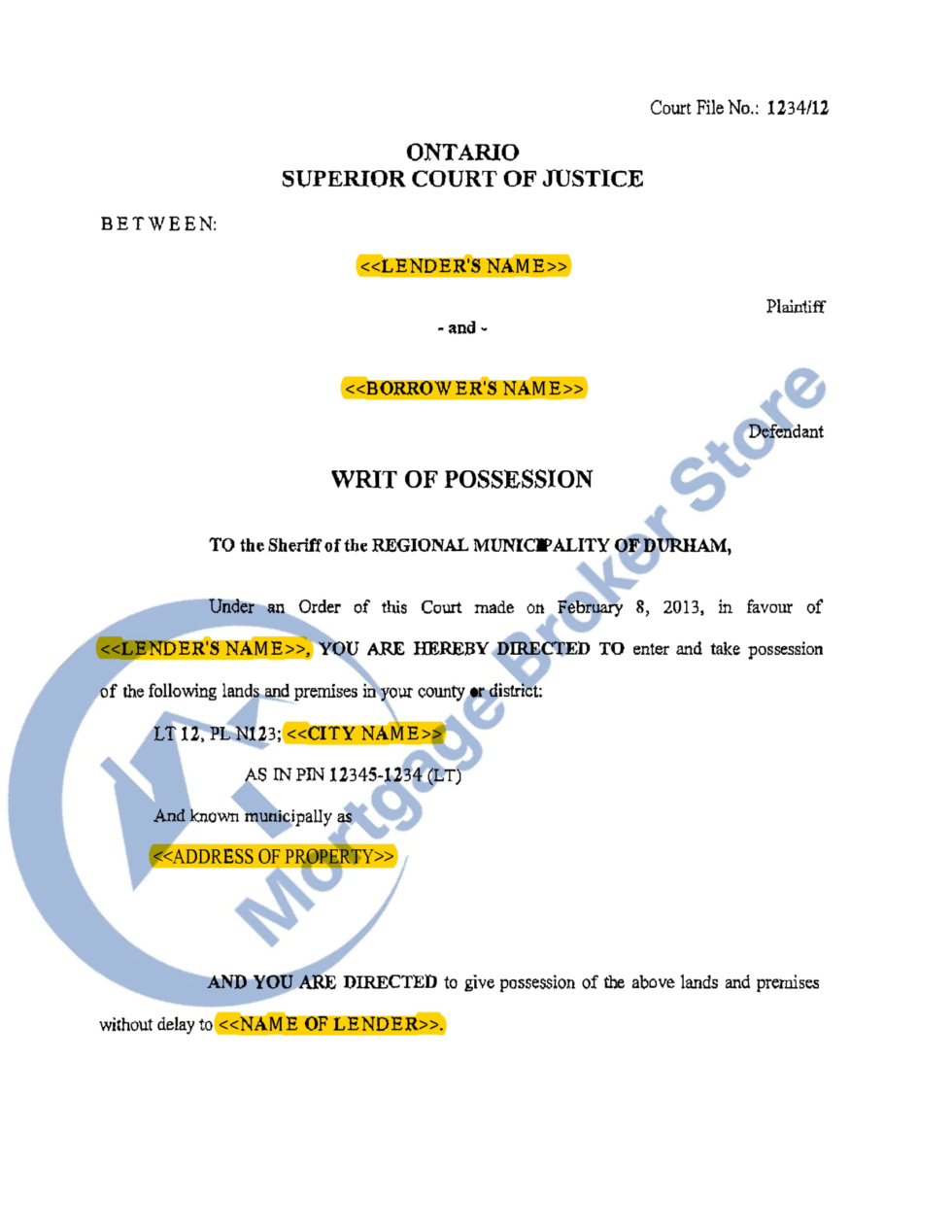

Writ of Possession

If the judge rules in favour of your lender, the judge issues a judgment for possession. A judgment for possession is a formal notice to the local Sheriff of the Power of Sale on your home.

Based on the writ of possession, the Sheriff issues an eviction notice.

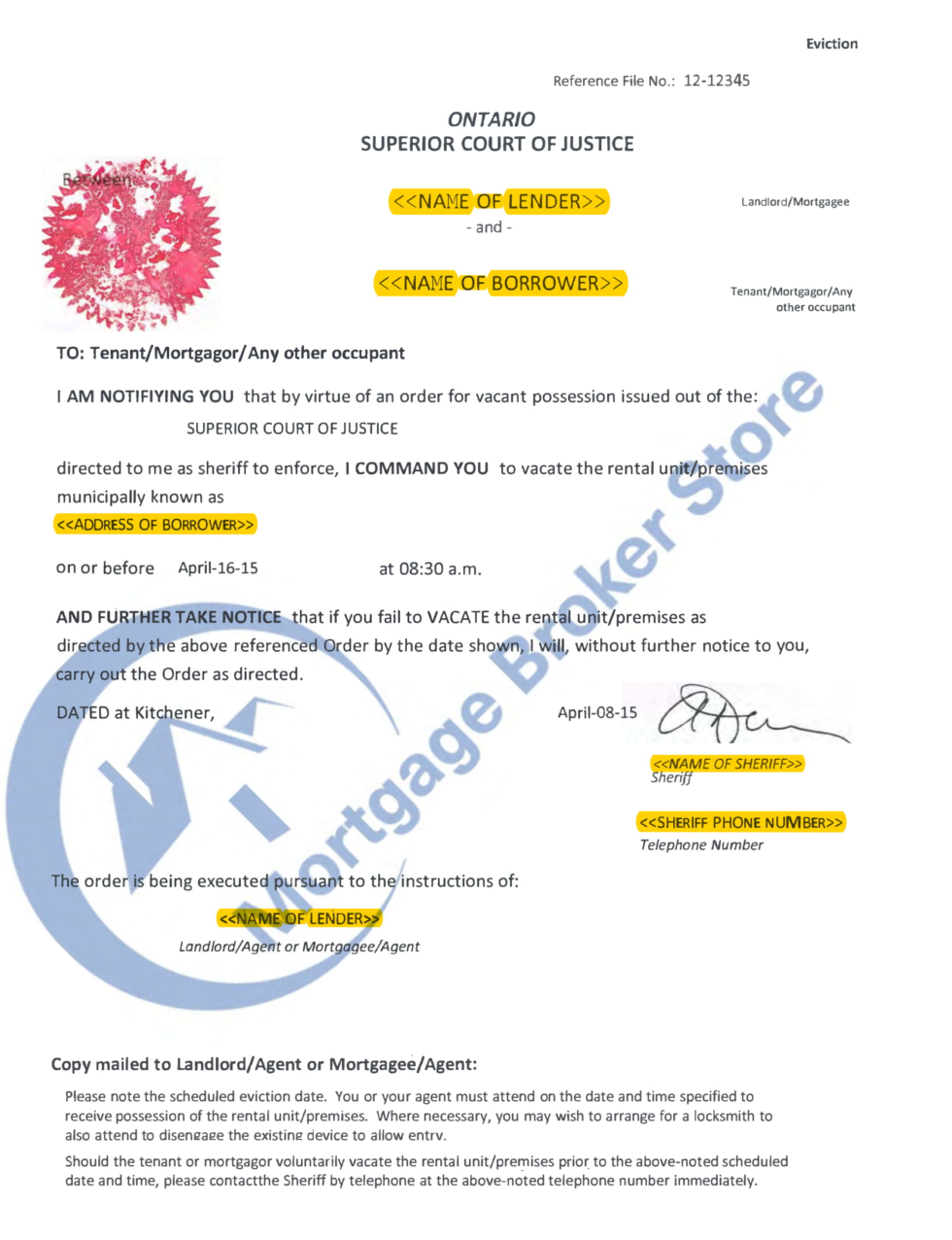

Eviction Notice

An eviction notice is the final step in the Power of Sale process. The eviction notice indicates how much time you have left to permanently move out from the home.

The sheriff can authorize police to remove anyone who disobeys an eviction notice.

The lender will sell the vacated property at market value. Once sold, the mortgage or loan is repaid, as well as any legal and real estate fees that were incurred during the sale. Any funds left after these payments will go to you.

Stopping Power of Sale in Ontario

If you are worried about the possibility of losing your home through Power of Sale, you are not alone. Canadians have deferred over $1 billion of mortgage payments each month since the pandemic began and a recent report from RBC found that 10% to 20% of all mortgage deferrals are at high risk of defaulting. If you think you are at risk of defaulting on your mortgage, the first thing you should do is review your monthly mortgage payments, essential expenses and expected earnings.

Having some money left after paying the mortgage and essential expenses each month can help you manage payments going forward.

If you realize you cannot maintain current payments, talk to your lender as soon as possible. Try to renegotiate the loan agreement for lower monthly payments. If negotiation is not feasible, you might consider a new loan to pay off your current mortgage, especially if a new loan results in lower monthly payments. Private lenders can approve loans like mortgage refinancing that only require interest payments to be made each month.

Of course, pre-emptively selling your home will also avoid a Power of Sale and avoid additional costs charged by the lender during a Power of Sale.

As with any legal process, it is beneficial to seek the advice of a lawyer in order to protect your interests. A financial advisor can also be consulted to help you understand your financial options and improve your financial situation. For support and more information, email ron@mortgagebrokerstore.com or call 416-499-2122.