Statistics on Mortgage Arrears in Canada for 2022

Last updated:

What Are Mortgage Arrears?

Mortgage arrears are the missed or late payments on a mortgage loan. Mortgage delinquency or default happens when the borrower fails to make the monthly payments as agreed upon in the mortgage agreement. It is essential to adhere to the terms of the agreement to avoid any legal repercussions. Mortgage arrears in Canada for 2022, left unpaid, can result in the lender’s power of sale or foreclosure of a property.

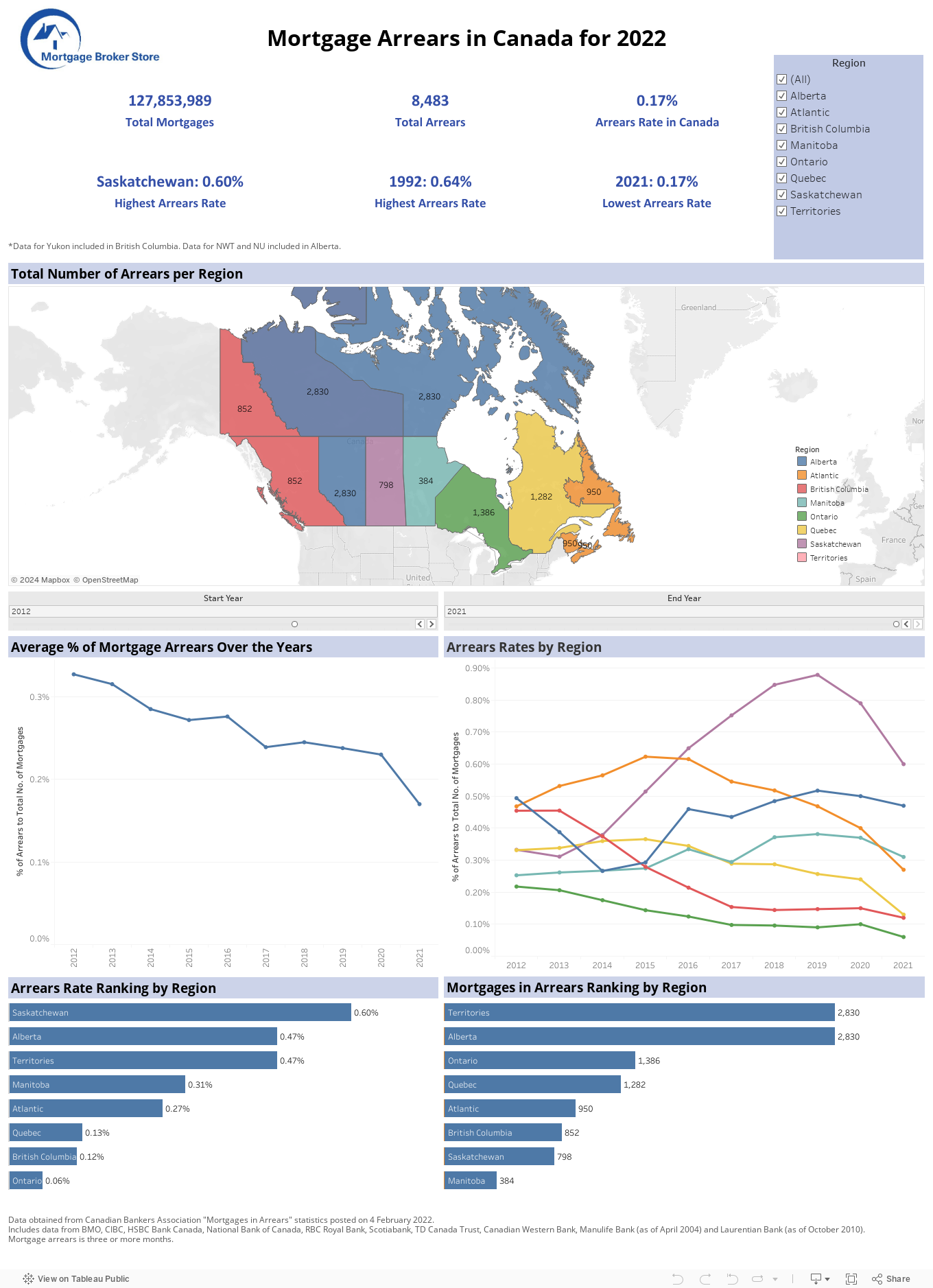

The Canadian Bankers Association released their latest statistics in February 2022, reporting that 0.17% of the total mortgages in Canada are delinquent— that is 8,482 out of 5,022,143 in Canada as of the end of November 2021.

Per region it is Saskatchewan with the highest percentage of arrears to total mortgages with 0.60%, followed by Alberta (including Northwest Territories and Nunavut) at 0.47%, Manitoba at 0.31%, Atlantic (including New Brunswick, Nova Scotia, Prince Edward Island, and Newfoundland and Labrador) at 0.27%, Quebec at 0.13%, British Columbia at 0.12%, and Ontario being the lowest at 0.06%.

The reason for Canada’s arrears rates going historically low would be the record-breaking price hike and increasing buyer demand. This seller’s market became a way for borrowers in distress to sell their homes and pay their remaining balances.

Good thing it was the opposite of what the Bank of Canada predicted back in 2020 when they expected more Canadians to default on their payments due to the extraordinary economic impact of the Covid-19 pandemic and people were paying medical bills on top of job losses.

Data from the Canadian Bankers Association

The Canadian Bankers Association released the latest “Mortgages in Arrears” report on February 4, 2022, detailing Canadian mortgage statistics. It contains data from BMO, CIBC, HSBC Bank Canada, National Bank of Canada, RBC Royal Bank, Scotiabank, TD Canada Trust, Canadian Western Bank, Manulife Bank (as of April 2004) and Laurentian Bank (as of October 2010). In this report, mortgage arrears in Canada for 2022 are those three or more months in delinquency. Data for Yukon is included in British Columbia. Data for Northwest Territories and Nunavut is included in Alberta.

What Impacts the Arrears Rate?

A borrower defaults when they are unable to pay their debts. Generally, our most significant debt is our mortgages, the most challenging debt to pay off fully. The pandemic halting the economy caused significant worry, especially for those reliant on regular paychecks to sustain themselves.

The Bank of Canada did a study to understand the rate of mortgage arrears. This study saw the relationship between climate change and financial stability by observing the Fort McMurray case study. They observed that “The economic impact of COVID-19 is often compared with past recessions, but this pandemic arguably has more in common with natural disasters. Natural disasters and pandemics both halt economic activity abruptly due to external shocks, like a public health crisis. The 2008 recession revealed global financial fragility, leading to a prolonged downturn, unlike the current situation.”

Policies aimed at supporting households have a direct impact on the ability of borrowers to make their mortgage payments on time, such as:

- Direct income support – by the Canada Emergency Response Benefit (CERB), Enhancement to Canada Child Benefit (CCB), Various programs at the federal, provincial, and territorial levels.

- Mortgage payment deferrals – Up to six months for COVID-19.

- Tax relief – CRA taxpayer relief provisions, Increased tax credits for COVID-19.

- Expedited employment insurance (EI) claims – Redirection of EI claims to the new CERB system for COVID-19.

For the household borrower, the extent to which they will default on their mortgage during this pandemic would depend on:

- Their financial health when the pandemic started

- The effectiveness of policy actions aimed at bridging the road to recovery

- The speed at which the labour market recovers

Contact us at jonathan@mortgagebrokerstore.com or 416-499-2122 for mortgage assistance tailored to your financial situation and credit goals.

This article is provided for educational purposes only and does not constitute mortgage, legal, tax, financial, or investment advice. Mortgage products and lending criteria vary by lender and borrower circumstances. Readers should seek professional advice before making financial decisions.

Flexible mortgage solutions for complex situations.

Speak with a mortgage specialist about private lending, refinancing, debt consolidation, or urgent property-sale options.

- A specialist reviews your situation directly.

- You get practical options for the next step.

- No obligation and no hard credit pull from this form.

Request a mortgage review

Share the best way to reach you and a specialist will follow up directly.

Private, no obligation, and handled by the Mortgage Broker Store team.